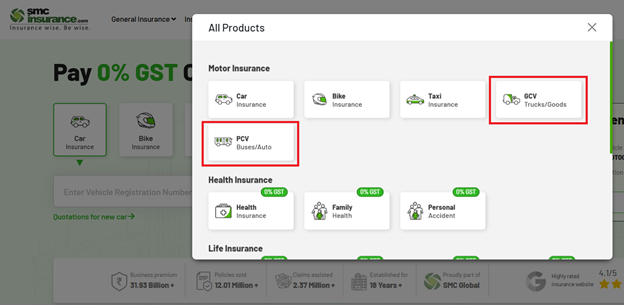

Visit the SMC Insurance Brokers Official website and click on the “View All” option..

100% Privacy

Zero Spam

Network

30+ Reliable Insurers

Legacy

20+ Years & Counting

Highly rated insurance website

4.1/5

Plans start at Just ₹19.92/day

For many owners and drivers, an e-rickshaw is how the day starts and how money comes home. Every ride means passengers, traffic, narrow turns and long hours on the road. And on Indian roads, no day is fully predictable. That’s why e-rickshaw insurance matters. It protects you when an accident happens, when your vehicle gets damaged, or when something goes wrong beyond your control. At the very least, third-party insurance is required by law. But for many drivers, basic cover is not enough.

A good e-rickshaw commercial insurance policy helps pay for repairs, covers damage to others and supports you during unexpected losses like theft or floods. When chosen right, it reduces financial pressure and helps you get back on the road faster. This guide explains e-rickshaw insurance in clear, everyday language, so you can choose a policy that actually works for your daily driving life.

The Motor Vehicles Act of 1988 requires commercial passenger vehicles to carry valid commercial vehicle insurance. If you carry people for hire, the bare minimum is third-party cover. That protects people and property you might harm in an accident. Driving without it risks fines, penalties and personal exposure to large claims. Many owners find that the real value of a policy is not legal compliance alone. It is the financial certainty that a serious accident will not wipe out weeks or months of earnings.

Let’s now look at the two types of insurance that you can buy for your e-rickshaw:

Premiums combine a few clear elements:

The IRDAI publishes third-party rates for categories such as e-rickshaws. That gives a predictable base price you can rely on when budgeting.

Insurers use the Insured Declared Value or IDV, which reflects market value. A higher IDV raises the comprehensive premium.

Zero depreciation, engine protection, roadside assistance, legal aid for disputes. Each increases the premium.

A clean record earns a no-claim bonus and lowers renewal premiums.

Commercial use raises risk compared with private use. Insurers price accordingly.

Garaging location, theft risk in the area and safety devices can affect some offers.

When you get a quote, ask for a clear breakup. That helps you compare apples to apples.

The Insurance IRDAI keeps motor third-party premium schedules public. These documents list base premiums and passenger charges for categories including e-rickshaws. That means though comprehensive premiums can vary by insurer and add-ons, the minimum third-party numbers remain steady and transparent. Checking the IRDAI’s rate notice is a quick way to verify quotes you receive.

Insurer pages that sell e-rickshaw cover also list the current third-party numbers and example premium calculations. These pages help owners see how the per-passenger charge adds up if the vehicle carries multiple licensed seats.

Useful Resource: Recent IRDAI guidelines for three-wheeler insurance

Some add-ons are especially practical for daily commercial use:

|

Add-On Cover |

Protection |

|

Zero Depreciation |

On a claim, the insurer pays the full cost of replaced parts without deducting for depreciation. Valuable for older vehicles or when parts are costly. |

|

Engine Protection |

Covers engine repair or replacement from leakage or water ingress. Useful if your route crosses waterlogged streets. |

|

Legal Liability to Paid Driver |

If you employ a driver and they are injured in an accident, this can extend cover. |

|

NCB Protection |

Protects your no-claim bonus in case you need to make a claim once. It keeps renewal discounts safe. |

Remember to only pick add-ons that match real risks on your route. Add-ons add cost but reduce surprises.

To buy a policy or file a claim, keep these ready:

Having these documents ready speeds up claims and renewal. It’s important to note that insurers may ask for additional proof depending on the claim.

Buying and renewing are both straightforward today if you use a comparison platform:

If you want help comparing offers, you can use platforms that partner with many insurers to show several plans. That makes it easier to spot the best price and the most fitting cover.

If you face an accident or theft, follow these steps:

Doing each step promptly improves the chance of a smooth settlement. Keep copies of everything.

When your e-rickshaw gets damaged and you raise a claim, the insurer usually gives you two ways to get the vehicle repaired. The difference is mainly in who pays first and how much paperwork you handle. Let’s break both in a simple way.

Here’s how cashless repair usually works:

However, cashless claims can be tricky:

Here’s how reimbursement works:

Some downsides of reimbursement include:

So, which one is better for e-rickshaw owners?

If your route is in a city or town with network garages, cashless is usually easier. If you work in smaller towns or rural areas, reimbursement may be more practical because local mechanics handle most repairs. This is why many experienced owners check the insurer’s network garage list before buying policy. That one step avoids stress later.

A few quick rules help pick the right policy:

Think of comprehensive cover as a cost for peace of mind. Third-party is a cost for legal compliance.

Here are some tips:

Always remember that small changes now can add up over the life of the vehicle.

Insurers sometimes reject claims for reasons that could have been avoided:

Follow the law, keep documents in order and report quickly to reduce the chance of denial.

Claim timing depends on three main things:

For commercial vehicles like e-rickshaws, insurers try to move fast because the vehicle is linked to daily income. Still, some claims need more checks than others. Below is a practical view based on typical industry timelines.

|

Claim Type |

What It Usually Includes |

Typical Processing Time |

|

Minor Damage Claim |

Small accident, body damage, light replacement, small parts repair |

2 to 7 days |

|

Moderate Damage Claim |

Major accident repair, multiple parts replacement, structure repair |

7 to 20 days |

|

Major Damage / Total Loss |

Vehicle badly damaged beyond repair |

15 to 30 days |

|

Theft Claim |

Vehicle stolen and not recovered |

30 to 90 days |

|

Third-Party Injury Claim |

Injury or property damage to another person |

Highly variable (can be months) |

You should make it a point to:

This checklist speeds purchase and avoids surprises at claim time.

And when you want to compare many insurers quickly, it helps to use a platform that works with multiple providers. At SMC Insurance, we show side-by-side coverage and price. If you prefer someone to handle paperwork and claims, a broker or an insurer with a local branch may help. Either way, check reviews and ask if they support cashless repairs and claim help on the phone. Use such a platform to see a variety of choices before you decide.

Some states require fitness certificates or route permits for commercial three-wheelers. Check your local transport office for any fitness tests and for registration class changes. A fitness requirement protects passengers and may affect which insurers will cover your vehicle.

A lot of small owners find that a single big repair bill can wipe out weeks of income. Comprehensive cover limits that risk. It also speeds repairs through cashless garages. If your e-rickshaw is new, comprehensive cover protects value. If you depend on the vehicle daily, the modest extra cost can be worth the peace of mind.

Getting commercial vehicle insurance through SMC’s website is quick and straightforward:

From the available options, select if your vehicle is GCV (Goods Carrying Vehicle) or PCV (Passenger Carrying Vehicle)

Once chosen, you will be taken to the respective page. You can use the on-screen widget and enter your vehicle number and click on “View Quotes”. This will directly take you to the commercial insurance buying process of SMC Insurance.

Fill in the required vehicle details. This includes vehicle category, brand, model, RTO location, and how long you want the policy to last.

Review quotes from multiple insurance partners and compare pricing and benefits side by side.

Customize your policy by adding optional protections like roadside support or engine cover, based on your needs.

Complete the payment online. Your policy documents are sent to your email soon after payment confirmation.

Download the policy from the SMC app or your email. Check all details carefully, then you’re set to drive with coverage in place.

Insurers now offer features aimed at commercial three-wheelers such as:

Here’s one last checklist for you:

Because, a little preparation reduces risk and keeps you legal.

With e-rickshaw insurance, you can keep your business running even after the unexpected. It protects passengers and your income. If you focus on the real needs like legal minimums, the likelihood of repair or theft on your route and the value of add-ons that match those risks, you can pick a policy that protects earnings without overspending.

When you are ready, compare current offers and read the policy wording carefully. If you want, use a multi-insurer platform like SMC Insurance to see options in one place and pick the cover that suits your daily route and income.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

(Showing Newest to Oldest)

Simple Process

The company is wonderful insurance platform providing multiple policies under 1 roof. Experience in purchasing the policy is very good. Experts guides you very well

Easy Renewal process

The process to renew my 2-wheeler policy is indeed very quick and easy. Got it done in just 10 minutes. Thanks.

Quick Response

I thought let me renew my two wheeler policy with SMC and see the experience. The experience was good and simple, the only gap which I felt was that the details of the vehicle did not come up after mentioning the vehicle number.

Yes, under the Motor Vehicles Act, 1988, every e-rickshaw operating on Indian roads must have at least third-party liability insurance. This is not optional. Riding without valid third-party cover can lead to fines and other penalties.

Common insurers that offer e-rickshaw or commercial vehicle insurance include Bajaj Allianz, Digit Insurance, Royal Sundaram, SBI General, New India Assurance, Reliance General, Tata AIG, ICICI Lombard, etc. These are among the established names selling commercial e-rickshaw policies.

You can visit an insurer’s website and enter vehicle details (reg number, model) to get a quote. Use an online insurance comparison portal like SMC to view prices from multiple firms at once. And premium is influenced by vehicle type, IDV, location, seating and add-ons chosen.

IRDAI sets base third-party rates (updated yearly):

These are fixed amounts for liability-only cover. Comprehensive policy costs vary by insurer and cover levels.

Click on an SMC Insurance official website or an insurance portal. Enter vehicle reg number, make and model, choose plan type (third party or comprehensive) and fill personal and vehicle info. Pay premium online and download the policy instantly.

Standard third-party insurance does not cover any part of the e-rickshaw itself (battery, motor, frame). Whereas comprehensive policies can cover your vehicle’s own damage, including battery/motor losses if that is included in the plan or with specific add-ons.

Login to the SMC website and just enter the vehicle registration number. The system fetches details so you can renew without phone OTP.

Yes, passengers are considered “third parties” under the policy, so third-party liability insurance covers passenger injury/death or loss in an accident.

Coverage types are the same (third-party or comprehensive). The only key difference is the premium rates and vehicle class tables, since e-rickshaws and auto-rickshaws fall under different tariff categories.

A third-party policy does not cover theft. Whereas a comprehensive policy will cover theft and loss if you choose that level of cover.

Common useful add-ons (for comprehensive plans) include:

These help extend protection beyond what a basic policy offers.

Typically required:

Exact list may vary by insurer.

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

SMC Insurance Brokers Pvt. Ltd.

SMC Metro Mall, Near Pratap Nagar Metro Station, Pratap Nagar, New Delhi-110007

Registration No: 289, Registration Code No: IRDAI/DB-272/04/289, Valid till: 27/01/2029, License category: Composite Broker, CIN: U66000DL1995PTC172311

Insurance is the subject matter of solicitation.

Visitors are hereby informed that their information submitted on the website may be shared with insurers.

Product information is authentic and solely based on the information received from the Insurer.